# What Healthcare Receivables Financing Is, What It Is not, and Whether It Fits Your Practice

Written by Emily Davis

What Healthcare Receivables Financing Is, What It Is not, and Whether It Fits Your Practice

Most practice owners have heard of factoring. Fewer have heard of healthcare receivables financing. The two sound similar. They are not the same. And the difference matters if you are thinking about using your A/R to smooth out cash flow.

What it is

Healthcare receivables financing is the sale of specific, submitted insurance claims to a financing partner in exchange for immediate cash. You submit a claim. The financier advances a percentage of the expected payment. When the payer settles, the financier collects and reconciles the difference.

At Copay, the rate is 0.75% for the first 10 days, with a daily rate after that. No minimums. No contracts. You access capital tied to specific claims, at the claim level, and reconcile when the payer settles.

The key distinction: this is not a loan. You are not borrowing against future revenue. You are converting an existing asset, your submitted claims, into cash today. The claim is the collateral. Your balance sheet does not take on debt.

What it is not

It is not traditional factoring. Traditional factoring sells your entire receivables ledger to a third party. The factor takes over collections, often communicates with your patients, and charges fees that compound over time. Healthcare receivables financing is claim-level, discreet, and designed around the specific dynamics of insurance reimbursement.

It is not a line of credit. A line of credit requires collateral, covenants, and often a personal guarantee. It sits on your balance sheet as debt. Receivables financing does not. The claim itself is the security.

It is not a billing service. We do not touch your billing process. We do not interact with your patients. We do not change your workflow. We advance on claims you have already submitted and verified.

How it compares to other options

| Option | Speed | Cost | Balance Sheet Impact | Flexibility |

|--------|-------|------|---------------------|-------------|

| Healthcare receivables financing | 24-48 hours | 0.75% for 10 days | None (not debt) | Claim-level, no minimums |

| Traditional factoring | 3-5 days | 2-5% monthly | None | Ledger-level, long contracts |

| Line of credit | 2-4 weeks to set up | 8-12% APR | Debt | Fixed limit, covenants |

| SBA loan | 60-90 days | 6-8% | Debt | Fixed amount, collateral required |

| Credit card | Immediate | 18-25% APR | Debt | Limited by credit limit |

For practices with $500K to $2M in monthly A/R, receivables financing is typically the fastest and most flexible option. For practices with strong banking relationships and time to wait, a line of credit may be cheaper on paper. The tradeoff is speed and flexibility versus absolute cost.

When it makes sense

Healthcare receivables financing fits practices that:

- Have predictable claim volume but unpredictable payment timing

- Need working capital for payroll, rent, or growth without taking on debt

- Want to avoid long-term contracts or minimum volume commitments

- Prefer to maintain control of their billing and patient relationships

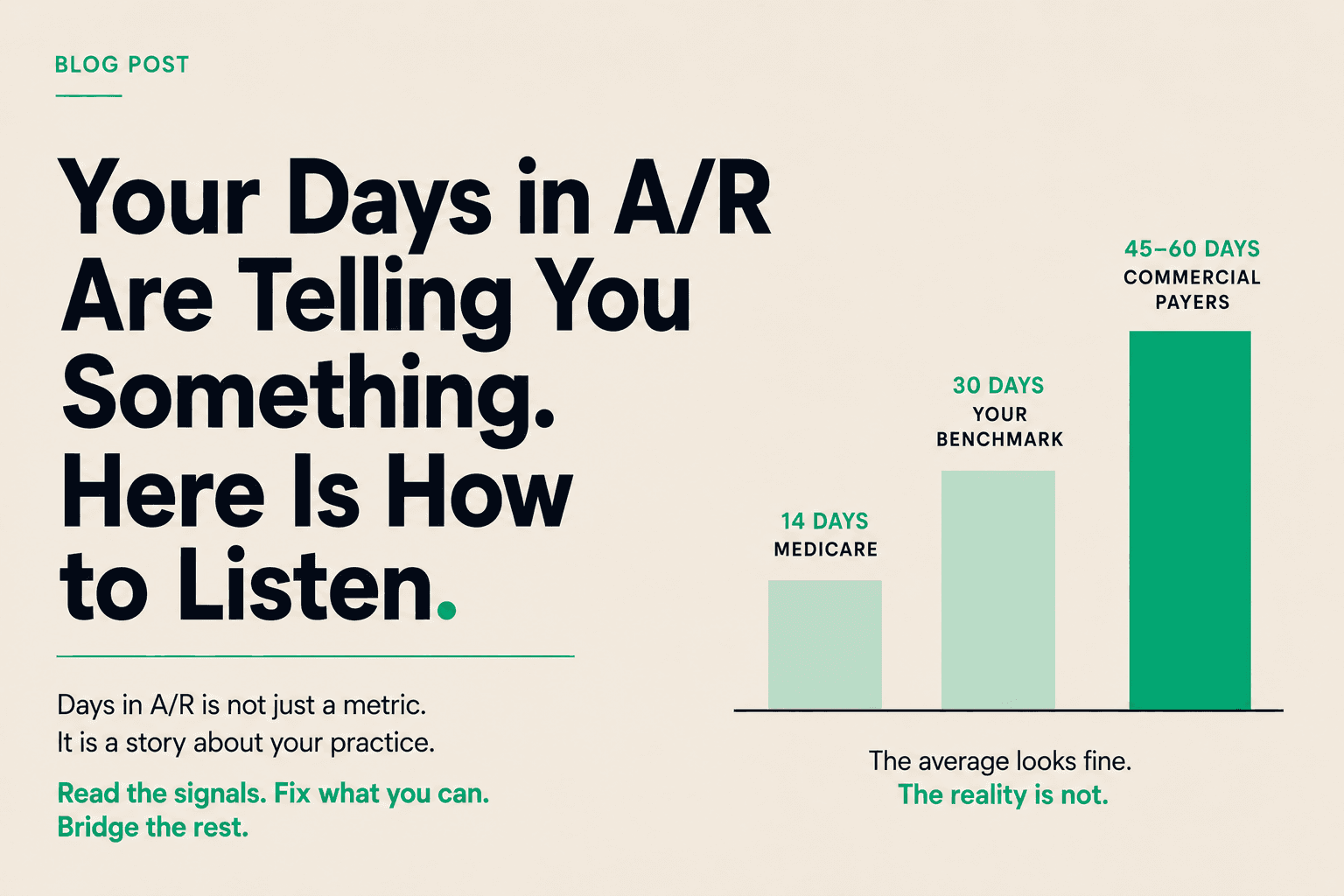

It is particularly useful for practices with a high commercial payer mix, where payment timelines stretch 45 to 60 days, or for practices growing faster than their cash flow can support.

When it does not make sense

It is not the right fit if:

- Your days in A/R is already under 20 and stable

- You have a strong line of credit with favorable terms

- Your claim denial rate is high (above 10%), which makes advance rates less predictable

- You need capital for a large one-time purchase (equipment, real estate), where a term loan is more appropriate

The bottom line

Healthcare receivables financing is a tool. Like any tool, it works best in the right context. If your practice has solid operations, predictable claim volume, and a cash flow gap created by payer timing rather than operational problems, it is worth exploring.

If you want to run the math on what your days in A/R is costing you and whether receivables financing makes sense at your volume, Copay is a good place to start.